Popular on Rezul

- Frost Locker: New Research Reveals Mild Cold—Not Extreme Cold—Delivers Real Health Benefits of Cold Therapy - 146

- Faith-Driven Books Empower Professionals to Build Businesses Rooted in Purpose and Integrity - 143

- Wzzph Deploys 5-Million-TPS Trading Engine with Hot-Cold Wallet Architecture Serving 500,000 Active Users Across Latin America - 142

- Phoenix Court-Appointed Realtor Releases Holiday Guidance for Divorce & Probate Home Sales - 141

- Divine Punk Announces Happy Christmas, a Holiday Soundscape by Rebecca Noelle - 139

- Sub-Millisecond Trading Platform: HNZLLQ Introduces Unified Gateway for Philippine Digital Asset Traders - 137

- Silva Construction Advises Homeowners on Smart Homes and Integrated Technology - 134

- Spencer Buys Houses Local Home Buying Service Focused on Speed, Fairness, and Simplicity - 132

- $2.1B Theft Losses: Bitquore Launches 1M+ TPS Platform with 95% Offline Asset Protection for U.S. Traders - 131

- Bookmakers Review Releases 2028 Democratic Nominee Betting Odds: Newsom Leads Early Field - 128

Similar on Rezul

- UK Financial Ltd Unveils The First ERC-3643 Security Token Born from a Meme: Introducing MayaCat Regulated Security Token (SMCAT) Successor to MayaCat

- Cybersecurity is Fast Becoming a Vital Issue for Protecting Personal Information and Portfolio Wealth

- Powering the Next Frontier of the $1 Trillion Space Economy: Ascent Solar Technologies (N A S D A Q: ASTI)

- Pioneering the Future of Human-Computer Interaction Through AI-Powered Neural Input Technology: Wearable Devices Ltd. (N A S D A Q: WLDS)

- American Star Guard Unveils a Powerful Rebrand and Expanded Security Services Throughout Nevada

- Flexible Plan Investments launches FlexDirex, a first-to-market suite of single-stock ETF strategies in the U.S

- Arnica Unveils "Arnie AI" to Secure the Future of AI-Driven Software Development

- $430 Million 2026 Revenue Forecast; 26% Organic Growth; $500,000 Stock Dividend Highlight a Powerful AI & Digital Transformation Story: IQSTEL $IQST

- Wzzph Deploys 5-Million-TPS Trading Engine with Hot-Cold Wallet Architecture Serving 500,000 Active Users Across Latin America

- $73.6 Million Multi-Year Backlog and Florida State Term Contract Drive Momentum for AI-Cybersecurity Pioneer: Cycurion, Inc. (N A S D A Q: CYCU) $CYCU

First Bancorp of Indiana, Inc. Announces Financial Results September 2025

Rezul News/10719646

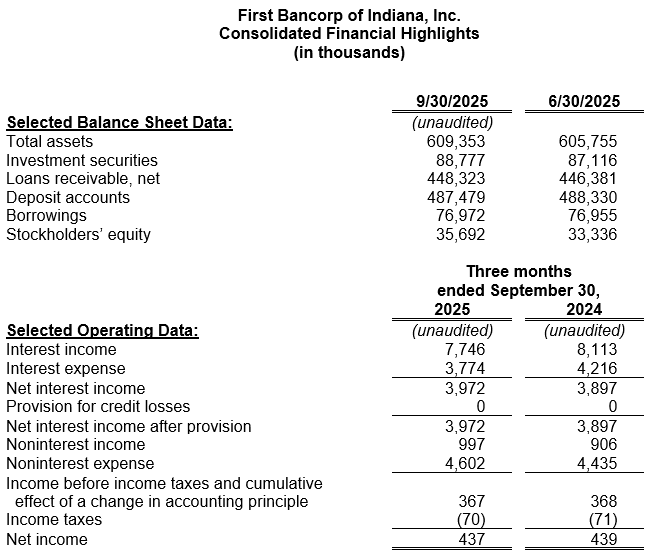

EVANSVILLE, Ind. - Rezul -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $437,000 ($0.26 per diluted common share) for the first fiscal quarter ended September 30, 2025, compared to $439,000 ($0.26 per diluted common share) for the same quarter a year ago. Earnings for the three-month period equate to a return on average assets ("ROAA") of 0.29% and a return on average equity ("ROAE") of 5.21%. This compares to an annualized ROAA of 0.28% and an annualized ROAE of 5.40% last fiscal year.

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on Rezul News

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on Rezul News

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on Rezul News

- Local Lighting Experts Debut AI Christmas Decorator: Upload a Photo, Get Instant Professional Holiday Design-- Completely Free

- Surf Air Mobility (N Y S E: SRFM) Accelerates Regional Air Mobility Revolution with Electra Aero Partnership, Palantir Alliance, and Record Revenue

- Cybersecurity is Fast Becoming a Vital Issue for Protecting Personal Information and Portfolio Wealth

- 10 Essential Tips for Maximizing Value When Choosing Your Orlando Wedding Venue

- Americans Are Trading Offices for Beaches: How Business Ownership Enables the Ultimate Location Freedom

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on Rezul News

- Boston Industrial Solutions' Natron® DC Series Ink Has Had an Upgrade!

- Colony Ridge Proudly Supports the All Ears! 2025 Sporting Clays Tournament

- Jacob Emrani Nominated for LA Executive Award

- Kansas City Steak Company Shares the Return of Their Holiday Gift Box

- Shiba Delivery Hits 100 Movers — and We're Just Getting Started

Source: First Bancorp of Indiana Inc

Filed Under: Financial

0 Comments

Latest on Rezul News

- POWER SOLUTIONS N.V. Partners with ENERGY33 LLC to Deliver a 40.5 MW Temporary Power Project for ECUACORRIENTE S.A. in Ecuador

- Pioneering the Future of Human-Computer Interaction Through AI-Powered Neural Input Technology: Wearable Devices Ltd. (N A S D A Q: WLDS)

- Epic Pictures Group Sets North American Release Date for the Action Thriller LOST HORIZON

- Local Roofer Homeowners to Protect Siding and Roofs Before Oklahoma's First Freeze

- Retired Firefighter Launches Family-Owned Home Inspection Company Serving Central Texas

- HR Soul Consulting Recognized as a 2025 Inc. Power Partner Award Winner for the Fourth Consecutive Year

- Resident Inspect Expands West Coast Reach Through Strategic Partnership with Real Estate Gladiators

- Central Florida Real Estate Market Sees Major Shifts

- Mark Wiesemann Awarded RE/MAX Lifetime Achievement Award

- Berkshire Hathaway HomeServices FNR celebrates the reopening of its Atlantic Beach office

- Brazil 021 Chicago Launches New Website and Expands with No-Gi Classes for All Levels

- American Star Guard Unveils a Powerful Rebrand and Expanded Security Services Throughout Nevada

- Tomball/Magnolia CRE Snapshot | Q3 2025

- Islamorada Key, FL: A Hotspot with Steady Demand for Investment Properties

- PlaceBased Media Expands Point-of-Care Advertising Inventory Across U.S. Clinic Network

- Be Home for the Holidays with Magnolia Green's Move-In Ready Homes

- Flexible Plan Investments launches FlexDirex, a first-to-market suite of single-stock ETF strategies in the U.S

- Denver Apartment Finders Unveils Redesigned Homepage to Help San Antonio Residents Relocate with Ease

- Realtor Trang Hooser and her husband David Hooser Treat their Team to All-inclusive Weekend

- Chris Fritch to Represent Minnesota on National TV Show "Minnesota Living: Beyond the Sale"